February 17, 2017

For the past eight years the Fed has been the driving force behind the economic expansion. But now President Trump has an unprecedented opportunity to re-shape the Fed’s Board of Governors. There are currently two vacancies on the Board. Fed Governor Dan Tarullo, who has been the Fed’s point man on financial regulation, intends to resign in the spring. Fed Vice Chairman Stanley Fischer’s term ends in June. And Fed Chair Yellen’s term ends in January of next year. That means that President Trump will have the ability to appoint the next Fed Chair, Vice Chair, and three Fed governors within a year. How might that alter the Fed’s conduct of monetary policy? Probably very little.

The markets currently fear that President Trump’s push for wildly stimulative cuts in individual and corporate income tax rates will produce much more rapid GDP growth and trigger a re-emergence of inflation. If so, the Fed would need to raise rates far more quickly than it currently envisions which could be the catalyst for the next recession. That fear is overblown. Despite changes in Fed leadership the Fed will continue on a slow but gradual path towards higher interest rates, the economy will continue to expand for several more years, and the expansion will ultimately go into the history books as the longest expansion on record.

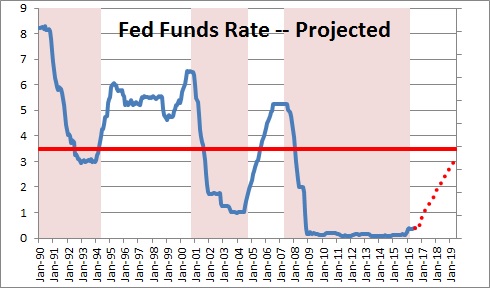

As the economy swooned in 2008 the Fed lowered interest rates to a record-setting low level of 0%. But now the Fed has decided the time has come to embark on a slow but steady path towards higher short-term interest rates. Why? Because it needs some leeway to lower rates at that point in time when the recession ultimately arrives. The Fed envisions the federal funds rate reaching a “neutral” level of 3.0% sometime during 2020. The direction of rates is clear regardless of who sits in the Fed Chair’s seat.

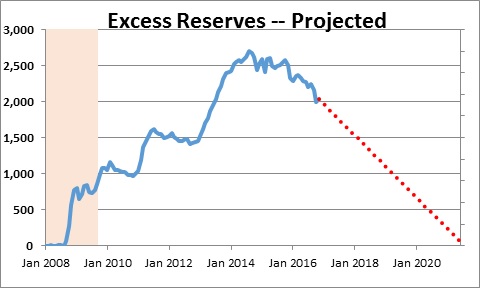

The second step in the Fed’s easing process in the wake of the recession was “quantitative easing” whereby it purchased U.S. Treasury bonds and mortgage-backed securities. In the process it flooded the banking system with more than $2 trillion of surplus reserves. Those “excess reserves” represent the lending ability of the U.S. banking system. If banks suddenly become willing to lend at the same time that consumers and businesses become more willing to borrow, those excess reserves could fuel an unprecedented, and highly inflationary, spending spree. Ultimately, those surplus reserves must be extinguished. One way to do that is to allow some of the Fed’s holdings of Treasury and mortgage-backed securities to mature and not be replaced. But such action is as contractionary as its bond buying spree was stimulative. To let securities run off at the same time that the Fed is raising short-term interest rates is not a good idea. While the Fed needs to shrink its balance sheet, this process will probably not begin for another year. But it is going to happen regardless who the Fed Chair might be.

The most important pick for President Trump is obviously the Fed Chairman. He could re-appoint Janet Yellen, but given his comments during the campaign about how she and the Fed were keeping interest rates artificially low in an attempt to support Hillary Clinton and the Democrats, the odds of that happening seem quite low.

The biggest challenges for the new Fed chair will be the speed with which interest rates will rise, and how soon the Fed will begin to shrink its balance sheet. It is not going to sit idly by and let the inflation rate climb. Why? Because in the past the Fed has let inflation get out of control and it paid a price for doing so. Inflation climbed to a double-digit pace in the late 1970’s as the Vietnamese War escalated. The economy overheated and the Fed (under Arthur Burns) refused to raise rates high enough or fast enough to prevent an upsurge in inflation. Ultimately, Paul Volcker had to push the funds rate above the 20% mark to break the back of inflation. The Fed will not let that happen again – regardless of who is in charge.

Keep in mind also that while Fed governors and the Fed chairman may change, the Board’s staff does not. These are people who have chosen a career at the central bank and are, in our opinion, extremely smart, capable and dedicated individuals. We have the greatest respect for the Board staff and are quite comfortable having it oversee the process of implementing monetary policy.

Some would like the Fed to implement a “rules-based” policy whereby rate changes are determined by formula rather than what some see as a rather arbitrary decision-making process. We strongly disagree with that concept. Models are based on history. As long as the structure of the economy does not change they may work well enough. But the economy is dynamic and constantly evolves. During the Great Recession consumers and businesses reassessed their attitude towards debt and are far less willing to hold debt today than at any time in recent history. Technological changes have made the economy far more reliant on the service sector today than in the past. Financial developments can result in never-before-seen instruments whose impact on the economy are unpredictable in advance. Reliance on a simple model to determine the course of monetary policy would be a disaster.

In our view, tax cuts of some magnitude will be adopted this year. However, with the prospect of $1 trillion budget deficits looming by the end of this decade President Trump will be unable to get Congress, or even Republicans, on board for untethered tax cuts. Some offsets in the form of reduced government spending will be required to temper the impact of the tax cuts. Hence, the economy will receive only mild stimulus this year, and the resultant increase in inflation should be relatively small.

Thus, regardless of changes in future Fed leadership, monetary policy for the next several years will not change much from what was described earlier – a moderate increase in interest rates followed by an eventual runoff of Fed holdings of U.S. Treasury and mortgage-based securities. If those things happen gradually the expansion is poised to become the longest expansion on record. It will hit the 10-year mark by June 2019. If the Fed can engineer a record-breaking length period of expansion, why in the world would anyone want to tinker with the process?

Stephen Slifer

NumberNomics

Charleston, SC

Good post. You have an error regarding the Vietnam War. It did not escalate in the late 1970s. It was over in April 1975. The great inflation of the 1970s had more to do I was told with Nixon’s abandonment of Bretton Woods in August 1971, which inspired the OPEC price hikes, which led to a flood of petrodollars into our banks. That’s all open to interpretation, I suppose. KP

Hi Kerry,

Thanks for your comment. You are correct about the date of the end of the Vietnam War. But, as I mentioned to you on the phone, it is my belief that it was the unfunded nature of that war that caused the double-digit inflation rate in the late 1970’s. We spend a lot of money on the war but were unwilling to raise taxes or cut spending enough to counter its inflationary impact on the economy. At the same time the Fed was unwilling to raise rates high enough or fast enough to bring inflation back down to a reasonable pace — until Volcker came along. I believe the Fed learned from that experience that it should never allow inflation to get so far out of line with their wishes.

Steve