October 4, 2024

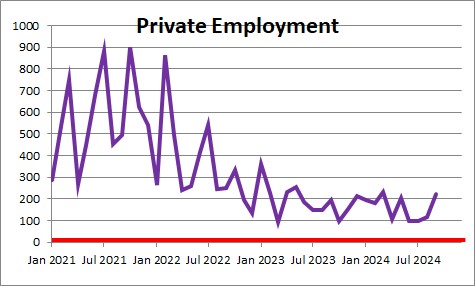

Private sector employment jumped by 223 thousand in September after having risen 114 in August.. In the past three months the average increase has been 145 thousand. The market had expected an increase in private sector employment for September of 140 thousand. There were also upward revisions to the employment data for June and July. Despite the September gain the employment gains still seem to be slowing down. However, jobs still seem to be climbing roughly in line with growth in the labor force which suggests that the labor market should be relatively stable in the months ahead.

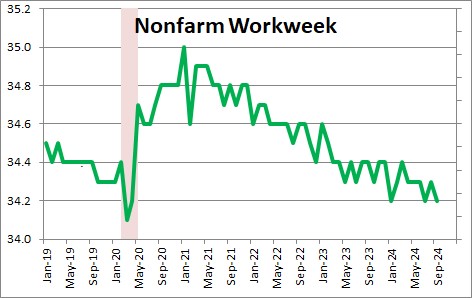

In addition to hiring workers employers can also alter the length of the workweek for their existing workers. The nonfarm workweek declined 0.1 hour in September to 34.2 hours after having risen 0.1 hour in August. Prior to the recession the nonfarm workweek was averaging 34.4 hours so it is weaker than it was four years ago. So while the labor market has softened it does not appear to be falling out of bed.

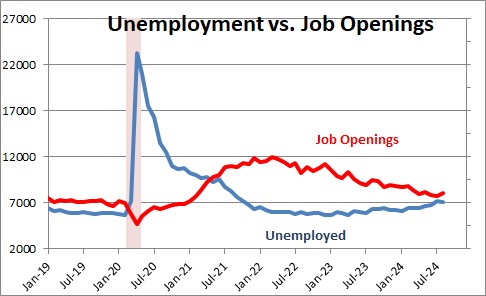

Job openings have fallen from a record high level of 11.7 million in early 2021 to 8.0 million. Prior to the recession there were about 7.0 million job openings per month versus 8.0 million currently. Today there are 1.1 job openings for every unemployed worker which is roughly where this was prior to the recession.

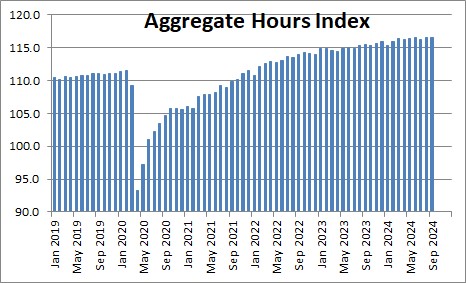

The change in employment and hours worked are reflected in the aggregate hours index which declined 0.1% in September after having risen 0.3% in August. This index rose 0.2% in the third quarter which we believe is reasonably consistent with our projected GDP growth rate of 2.0% in that quarter (because of an expected increase in productivity.

Construction employment rose by 25 thousand. Manufacturing employment declined 7 thousand. Retail trade jobs rose by 16 thousand. Transportation and warehousing declined by 9 thousand. Info tech jobs rose 4 thousand. Financial sector jobs rose by 5 thousand. Professional and business services gained 17 thousand. . Health care jobs climbed by 45 thousand. Social assistance climbed by 27 thousand. Leisure and hospitality jobs jumped by 78 thousand. Government jobs rose by 31 thousand almost exclusively at the state and local level.

Given these steady employment gains we expect GDP growth of 2.0% in the third quarter and 2.5% in the fourth quarter.

Stephen Slifer

NumberNomics

Charleston, S.C.

We have seen a change in the way companies are hiring employees. As the owner of the staffing company temp to hire has been a very popular strategy the last several years. Now companies are actually hiring people directly to their payroll and willing to pay fees. That would seem to indicate that they do not expect a downturn in the near future. Good news for all of us.

Thanks for the comment, Neil. From what you said, it certainly suggests that if they do expect a recession it will be short and mild and they will soon need those bodies. But what if rates really do need to go to 6% to slow things down enough to trigger the recession? The outcome may not be quite so mild. We will see.