March 7, 2024

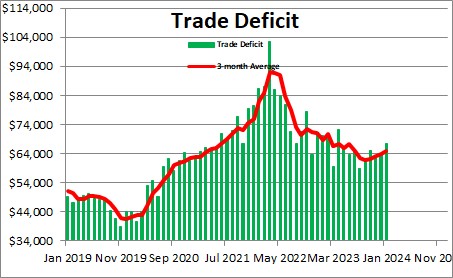

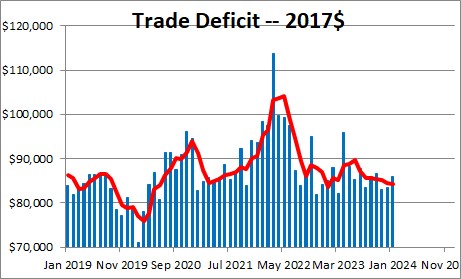

The trade deficit widened by $3.3 billion in January to $67.4 billion after having narrowed by $1.5 billion in December. t it has been largely unchanged during the course of the past year.

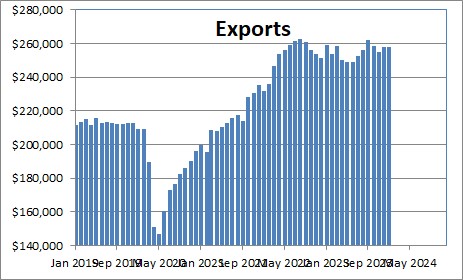

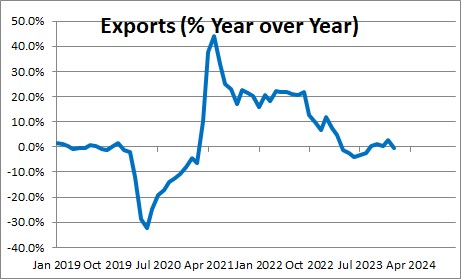

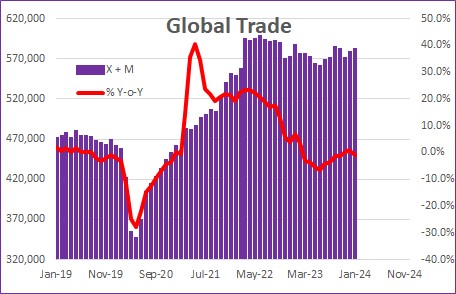

Exports rose $0.3 billion or 0.1% in January to $257.2 billion. It has been relatively steady for the past year. During that period of time exports fell 0.4%

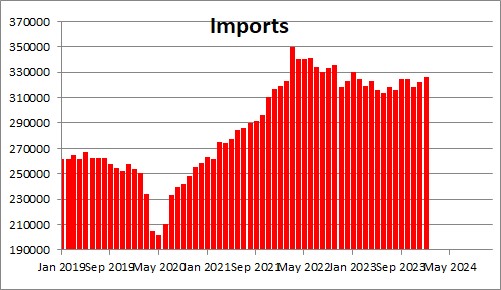

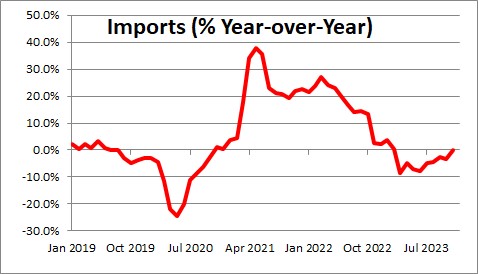

Imports rose $3.6 billion in January or 1.1%. In the past year imports have declined 1.2%.

The best gauge of global trade flows is the change in the total of both exports and imports. It, too, has changed very little during the course of the past year.

The trade deficit in real terms widened by $2.5 billion in January to $86.0 billion. The deficit in real terms is important because that is what goes into the GDP calculation. The trade component should have little impact on GDP growth in the first quarter.

Stephen Slifer

NumberNomics

Charleston, SC

Hi Steve,

I’m a bit confused, has the deficit increased so sharply as a result of overall reduced economic activity? Or is there some other factor at play here? Material costs? or? This seems surprising with the general weakness of the dollar.

Best,

Hi Chris what we are have seen in the recent trade data as well as what happened to trade in the first few months of the year were wildly distorted by the recession and subsequent rebound. The dramatic narrowing of the trade gap earlier did not mean a lot. Nor does the recent rebound. I guess the only point I was trying to make is that the increases in both exports and imports tells us nothing more than the rebound is underway with the recovery in the U.S. currently outpacing the rest of the world.

Ah, that makes sense.

Thanks